This is an article from the fall 2018 issue of LSA Magazine. Read more stories from the magazine.

A common joke calls Bitcoin “magic internet money,” which actually makes some sense. It works as digital money, but even easier, faster, more secure, and more anonymous than using online payment services with a credit card. Compared to dollar bills, the convenience of Bitcoin and other cryptocurrencies for things like sending money internationally or making micropayments online is like emailing a message instead of sending a stamped envelope.

In December 2017, the exchange rate of Bitcoin exploded to just over $19,000 per coin—compared to five years before, when one bitcoin went for less than $50 in the open market.

As Bitcoin’s popularity and notoriety grew, strange news involving unfamiliar trends such as CryptoKitties and Dogecoins added an air of levity and even illegitimacy to the whole enterprise. An illicit online marketplace, Silk Road, became infamous as a place to buy illegal drugs, a direct result of the security and anonymity of paying with Bitcoin. Investors lost hundreds of millions through failed Bitcoin exchange services, online heists, and scam imitation coins that hit the market.

In all this cryptocurrency hype and confusion, an LSA alumna became an investor.

Sam* (B.S. 2017) had a bright outlook with her LSA degree as a double-major in honors math and honors physics and was on her way to a Ph.D. program in physics at Stanford. But even as an undergrad at U-M, she stressed over the uncertainty of an academic profession and her financial future.

“I want to have a shot in academia,” Sam says, “but I know very well that most people who get a Ph.D. in physics won’t be able to find a faculty job.” Even with high hopes of making it as a professor, Sam anticipated several years of tight budgeting before getting there. One way she brainstormed to hedge her bets while still pursuing the research she loved was to get in on some cryptocurrencies.

“I just wanted to feel secure about my life, and I realized it would be good to put some of my pocket money into long-term investments,” Sam says. “I’m treating it like a bank with a weird rate of interest.”

Since early 2017, Sam has seen about a tenfold return. She chided herself as she checked on her holdings: “Why did I not put in more money?!” But she’s stayed calm and doesn’t plan to cash out anytime soon. At least, not until she’s done with grad school.

“It’s a life investment,” she says. “I’m a true believer with other believers around me, and we encourage each other. Even when the price goes down, we still hold our coins tight.”

“At the end of the day, the worth of Bitcoin depends on the value people ascribe to it,” says Lynette Shaw, an assistant professor in LSA’s Center for the Study of Complex Systems and a postdoctoral scholar in the Michigan Society of Fellows. “The question is whether you think Bitcoin will stick around and become more important.”

She says that belief in cryptocurrencies comes from various pockets of society. Positive perception derives in part from a faith in future profits by speculative investors. Other stakeholders include citizens in places like Zimbabwe, Argentina, and Greece, who don’t trust their countries’ currencies, along with political revolutionaries who place a premium on personal privacy.

The slippery definitions and diverse appeal gave a lot of different groups reasons to get interested and adopt Bitcoin, says Shaw, which helped drive up its value. “If it hadn’t been for the ability of different groups to do different things with cryptocurrency, it would not have spread to the degree it did in terms of adoption,” Shaw says.

As different camps started to put Bitcoin and other cryptocurrencies to good use, the corporate world did, too. Companies such as Microsoft, Overstock, Expedia, Dell, and Lamborghini have at various points accepted Bitcoin, partly because of its low-to-no transaction fees. In countries where rules restrict women from opening bank accounts, those women can turn to cryptocurrency, which requires no approval and no credit history.

Asheesh Birla (B.S. 2002), an LSA alumnus in economics and computer science, saw the promise of Bitcoin and of blockchain—the technology that makes cryptocurrencies work—to improve the process of sending money internationally. His parents emigrated from India to the Detroit area in the 1960s. “Sending money back home to our family was the most archaic process,” he says, “and it never got better.”

Birla’s parents could go to an Indian grocery store or use Western Union, but sending money through those routes took days and charged exorbitant fees. “If you sent $1,000, you’d get a fraction of it at the end of the day—maybe the equivalent of $800 over in India.”

Birla saw the same thing with his friends at U-M while he was a student. “With the diversity at Michigan, I realized when talking to international students how hard it was to get money into the United States.

“We take all this for granted. I have a couple of credit cards, but what about a new student who comes to the United States and Ann Arbor for the first time?” Birla says. “There are very low credit card penetration rates in India, Bangladesh, and a lot of Asia—it’s a big problem to move money.”

At U-M, Birla took all the computer science classes he could. He founded a company and sold it to Thomson Reuters after graduating, then struck out solo to explore opportunities in Bitcoin and blockchain in their early stages.

“They’re at the intersection of computer science and economics,” he marvels. “If I didn’t have the tech background from U-M, it would’ve been hard back in 2013 to realize why this was going to be such a radical new technology.”

Birla’s background led him to join the founding team of a company called Ripple, whose mission is to modernize global payments. Ripple creates products that help remove friction from cross-border payments, making international transfers reliable, fast, and inexpensive.

Now, with the growth of international businesses like Uber, Airbnb, and Amazon, which routinely transfer small payments, Ripple is well-positioned to help. “There’s no way to efficiently send a $200 payout for drivers when your fees are $40, no way to trace it, and it takes several days,” Birla says. “Those are problems that we really wanted to solve.”

Birla believes in the value of cryptocurrencies and blockchain technology so much, he says, “I’ve been in it for five years, and I’m planning on staying in it for the rest of my career.”

Jay*, an LSA senior studying economics, first encountered Bitcoin when he was in high school in 2014, running a business as an online merchant of virtual goods. “Nobody was going to pay a $25 bank wire fee to buy a $5 virtual sword in a game,” he says. Unlike a bank, Bitcoin demanded nearly no fees for transactions, and Jay took advantage.

At U-M as an undergrad, Jay grew curious about the blockchain technology underlying cryptocurrencies and took a course offered remotely by Berkeley. “I started thinking that we needed to find a way to spread that knowledge across our campus,” he says. Last year, Jay and four other U-M students started a group called Blockchain at Michigan.

“The strength of any public university is the sheer quantity of brilliant, motivated students who are looking to make an impact in the world,” Jay says. “The mission of Blockchain at Michigan is to build Michigan leaders in the blockchain space through education, research and development, and consulting. We’re focused on getting U-M students to actually build things, and eventually to place students in careers.”

Jay places a high value on blockchain technology. He’s writing a thesis about it and plans to build a career on it, too. He spent last summer in Chicago at an internship that helped him develop the skills he needs to keep innovating with related technologies.

“Everybody working with blockchain is passionate,” Jay says. “That’s something I find very unique about this space. Everyone is super energetic, and they all want to see it grow.”

Ideas about theoretical currencies are all well and good, but when it comes to money—digital or otherwise—most of us want to know one thing: what it’s worth. Should we hoard Bitcoin or ignore it? Are these cryptocurrencies really worth anything?

Well, is anything really worth anything?

“A lot of people believe the dollar is backed by gold, but that hasn’t been true for a long time,” Shaw says. “In fact, former President Richard Nixon announced in 1971 that U.S. dollars could no longer be redeemed for gold. When was the last time you could walk into a store and pay using a block of gold, anyway?

“I’d argue that to succeed as money,” says Shaw, “cryptocurrency has to become like a U.S. dollar or designer handbag, where people take its worth for granted—the point at which, collectively, we start to automatically treat its perceived value as reality.”

She admits that it’s tough to predict the future of Bitcoin and other cryptocurrencies. Bitcoin could become a routine currency; or fail as money but survive as blockchain technology; or boast the dubious legacy of a huge, expensive folly.

But cryptocurrencies already have demonstrated some kind of value, especially compared to the creaky payment infrastructure first built in the 1960s and ’70s. That system involves bureaucracy and hefty fees to track and approve payments, but the global community nonetheless continues to use it. People don’t hype Bitcoin and other cryptocurrencies because the digital coins have some inherent value; cryptocurrencies have value because people have found that they’re useful.

“In the everyday course of living,” Shaw says, “we forget that the value of such things is created and reproduced through our own actions and understandings.”

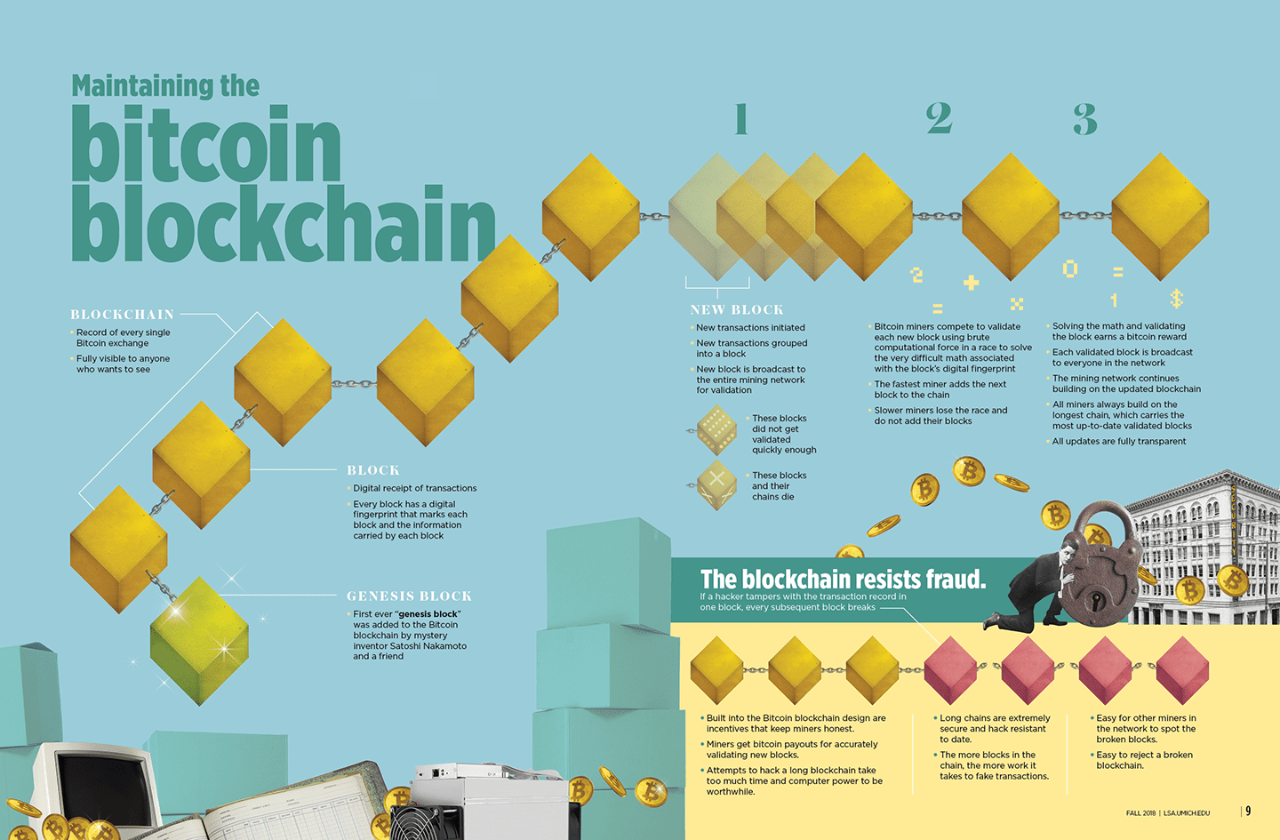

Click here to download a PDF of this infographic, which shows how blockchain technology works.

| Release Date: | 05/21/2018 |

|---|---|

| Category: | Research |

| Tags: | Physics; Economics; Mathematics; Natural Sciences; LSA Magazine; Complex Systems; Elizabeth Wason; Computer Science |